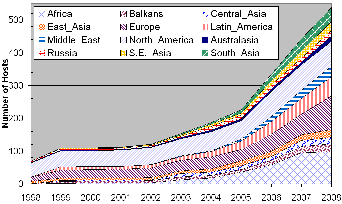

PingER

Links Connecting Africa

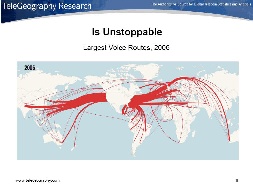

Voice Routes 1997 |

Voice Routes 2007 |

World Cables 2007 |

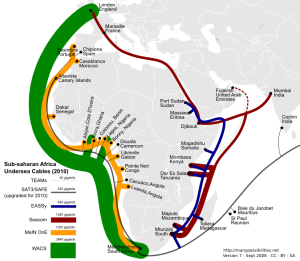

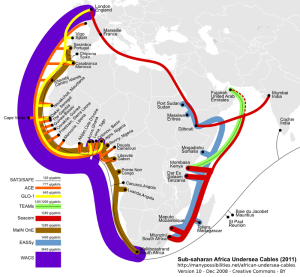

Africa Cables 2006-2008 Plans |

|---|---|---|---|

|

|

|

|

(c) manypossibilities.net - current |

(c) manypossibilities.net - current |

|---|---|

|

|

Satellite vs Fibre

Satellite is extremely effective in reaching places where the volume of traffic would not justify a fibre connection. Satellite providers are reluctant to talk about prices (except directly with their customers) because it is often difficult to explain to new customers that the lowest prices are only available to large customers with long contracts. However, if pressed satellite operators will say that below US$1800-2000 per mbps per month is not likely to be commercially feasible for them. (See Fibre for Africa).

Satellite networks are often severely bandwidth-constrained and possess high latency. Links may be as narrow as 64K and possess latencies of 250, 500, 750 milliseconds or more. This combination of conditions often leads to congested satellite connections and performance so poor that applications frequently time out. One can attempt to address the delays by improving TCP by increasing buffer sizes to accomodate the long delays), modifying its congestion algorithm. One can also compress data and/or use streaming.

Cell Phones vs internet

Despite efforts to provide high-speed Internet Africa is falling behindthe rest of the world. Due to lack of infrastructure many African countries concentrate on mobile phones. Hoever, this does not necessarily remove the need for bandwidth for as quoted by Network World 2/11/2009:

Cisco says the advent of smartphones and laptops with 3G aircards will lead to an explosion of mobile data traffic over the next five years, as an iPhone typically generates 30 times the mobile data traffic of a basic-feature phone, while a laptop generates 450 times the mobile data traffic as a basic-feature phone. A recent study by mobile browser developer Opera Software showed that data traffic sent to mobile phones jumped 463% in November 2008 as compared with November 2007, and that page views on mobile devices were up by 303% over the same period. Thus the need for bandwidth continues even wit just mobile phones.

Complex mobile applications, such as telemedicine, interactive gaming and mobile education systems, won't be realistically available until carriers begin launching more of their 4G network offerings next decade.

Further (from "Global Market Brief: Communications Inftastructure for the Developing World" Stratfor, 2/21/2008):

While mobile phone infrastructure is cheaper to construct, the fiber-optic lines are what attracts long-term investment from the business community, which needs dependable, high-speed and high-data-throughput telecommunications infrastructure at a globally competitive price. Consumer products businesses also see growth in the southern African region in offering high-tech, high-bandwidth products such as high-definition television, peer-to-peer file sharing and Internet TV.

Between 1999 and 2004, the number of cell phone subscribers in Africa jumped from 7.5 million to 76.8 million (translating to about one in 11 Africans having a cell phone), and one-fifth of these subscribers live in South Africa. The market grew about 58 percent annually during that time period, compared with the Asian market, which grew at about 34 percent annually during the same amount of time.

However from http://blog.ted.com/2007/07/incremental_inf.php

You can build a mobile phone network one piece at a time. With a GSM license and a single tower, a company can begin earning revenue and start using this revenue to finance future expansion. An investment in the single-digit millions can turn into a multi-billion dollar business through reinvestment of revenues. That just isn't true for creating container ports, major roads or large power generating facilities (...)

And from http://www.mbendi.com/indy/cotl/af/p0005.htm:

The world might be in recession but the African telecommunications sector continues to boom, fuelled by privatisations, liberalisation, new cell-phone services and infrastructure projects - some funded by the World Bank, African Development Bank and other agencies, but more funded by innovative entrepreneurs in partnership with international telecoms companies.

Although cable connections across many African countries are in a poor state of repair or non-existent, the continent is slowly being connected to the global community through five undersea cable projects, three of which are due for completion in 2009.

The African cell-phone sector is the fastest growing in the world, with subscription growth between 2007 and 2008 at 41% annually. Cell phones currently account for 90% of telephone subscribers in Africa. At the beginning of 2008, there were 300 million mobile subscribers on the continent.

Also in the developing world, said Mongi Hamdi, Head of the Science, Technology and Internet and Communications Technology branch of the United Nations Conference on Trade and Development:

"there are now estimated to be eight times as many mobile phones as fixed lines, three times as many mobile phones as personal computers, and nearly twice as many mobile phones as TV sets."

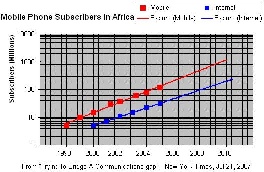

Taking the figures in http://www.nytimes.com/imagepages/2007/07/21/business/22rwanda_graphic.html and assigning values by eye one can plot them as seen below. There it is seen that Mobile penetration is about three times as great as Internet penetration, they are both growing at roughly the same rate, and Internet penetration is about 4 years behind the Mobile penetration.

Mobile vs Internet Subscribers for Africa |

|---|

|

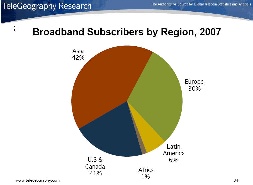

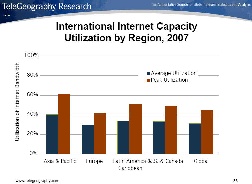

Regional Comparisons

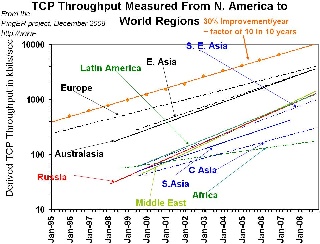

Inter Regional Traffic |

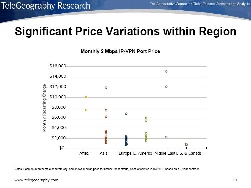

Price Variation |

Subscribers |

|---|---|---|

|

|

|

Utilization of Available Bandwidth |

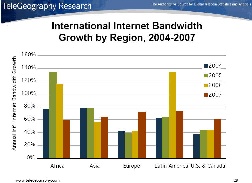

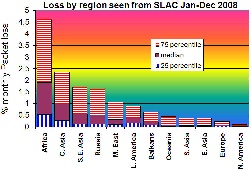

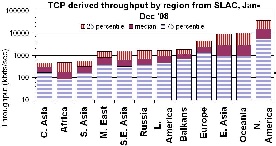

Growth by Region |

|

|---|---|---|

|

|

|

Loss Map |

Min-RTT Map |

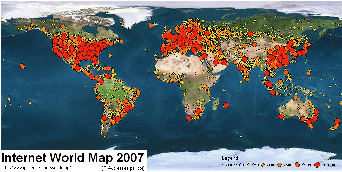

Internet World Map '07 |

Population Density people/sq-km |

Areas |

|---|---|---|---|---|

|

|

|

|

|

Loss variability |

Throughput variability |

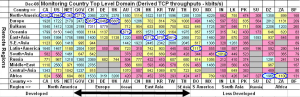

Region to Country Throughputs |

Region to Country Throughputs |

|---|---|---|---|

|

|

|

|

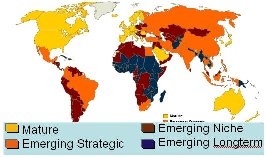

Given the saturation of many developed markets there is considerable attraction to exploring emerging markets, especially those with young populations.

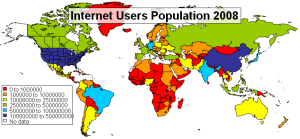

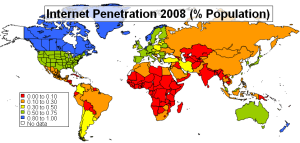

Internet Users Population 2008 |

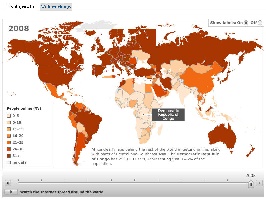

Internet Penetration 2008 (% Pop) |

Emerging Markets (Vital Wave) |

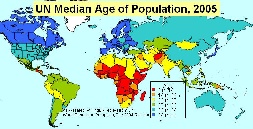

Population Age |

|---|---|---|---|

|

|

|

|

Trends

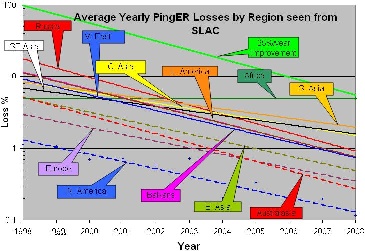

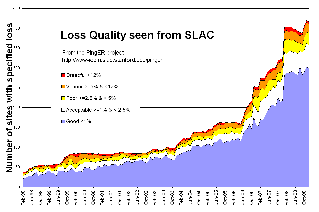

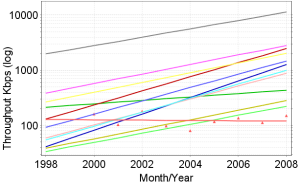

Throughput from SLAC |

Loss from SLAC |

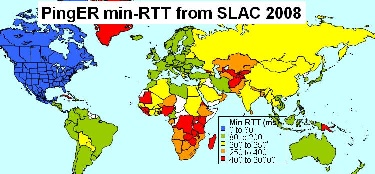

Minimum RTT from SLAC |

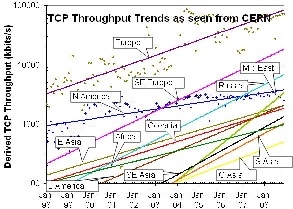

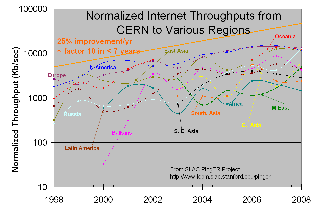

Throughput from CERN |

|---|---|---|---|

|

|

|

|

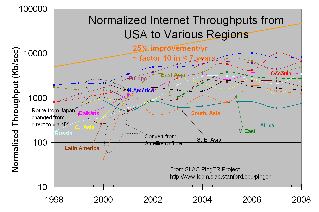

Normalized Throughput as |

Normalized Throughput as |

|---|---|

|

|

Cell Phones

Miscellaneous Statistics

Loss Quality as seen from SLAC |

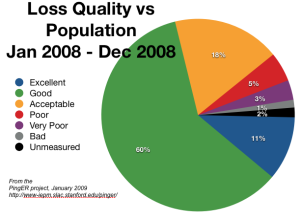

Loss Quality vs Population |

|---|---|

|

|

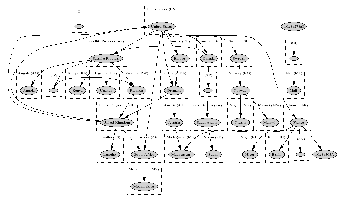

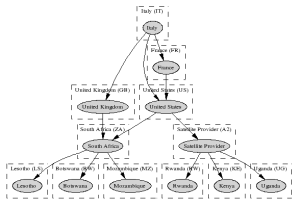

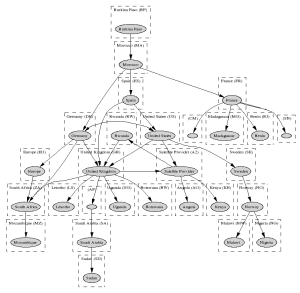

Routing to and within Sub-Saharan Africa

Revised: January 15th, 2009.

Generated by: PingER Route Visualizer

As seen from SLAC, |

As seen from NCP |

As seen from ICTP |

|---|---|---|

|

|

|

As seen from Bolivia, |

As seen from OUAGA, |

As seen from TWAREN, |

|---|---|---|

|

|

|

As seen from AARNET, |

As seen from KHU |

As seen from ACMESECURITY |

|---|---|---|

|

|

|

As seen from |

|---|

|

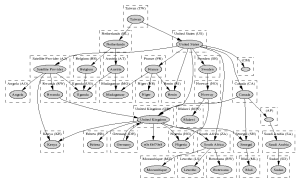

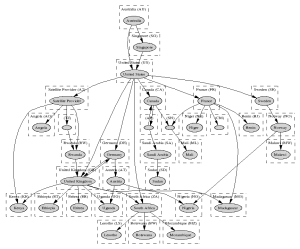

The same information is available in tabular format. We derive the conclusions listed below from the traceroute results gathered from monitoring sites located in Australia, South Korea, Taiwan, Pakistan, Burkina Faso, South Africa, Great Britain, United States, Mexico and Bolivia.

- East and Central Africa is mostly connected via satellites.

- Most of the routes in this case are via US. For example traffic to Angola transits via UK, US and a Satellite provider. Same is the case for countries such as Rwanda and Uganda.

- Access to Sudan is extemely poor. The routes from all monitoring sites mostly transit via US>CA>CN>SA or GB>US>NL>SA. For example, access from Burkina Faso is via Morocco, Spain, Great Britain, China and finally Saudi Arabia.

- Cameroon is the only country which is accessible via short short routes due to direct connectivity with France.

- Connectivity from the world isn't as bad as it is within the region. The lack of IXPs is evident from the fact that Burkina Faso has Nigeria, Benin, and Mali as neighbours, yet the traffic transits via Morocco>Germany>US>Sweden>Norway, Morocco>France and Morocco>France>Ivory Coast respectively.

- However there are exceptions such as South Africa being directly connected to Botswana, Lesotho and Mozambique.

- Other than that traffic is generally routed via US, GE, GB or US, SW, NO.

- Routes to countries such South Africa, Senegal, Mozambique and Cameroon are direct.

PingER Performance Metrics

MinRTT, AvgRTT, Packet Loss, |

Derived Throughput (Kbps) |

|---|---|

|

|

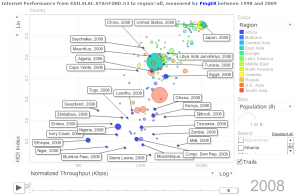

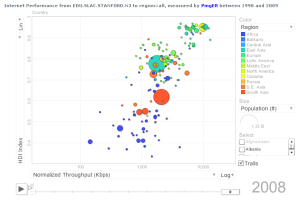

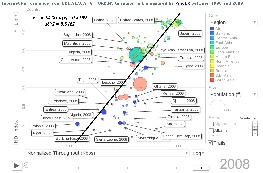

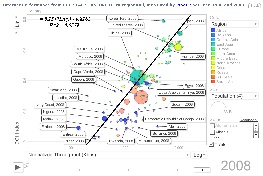

Performance Metrics VS Human Development Indices

Normalized Throughput VS HDI |

Normalized Throughput VS HDI |

Normalized Throughput VS HDI |

Normalized Throughput VS HDI |

|---|---|---|---|

|

|

|

|

Normalized Throughput VS DOI |

Normalized Throughput VS DOI |

Normalized Throughput VS DOI |

Normalized Throughput VS DOI |

|---|---|---|---|

|

|

|

|

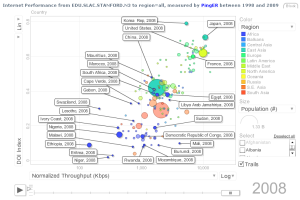

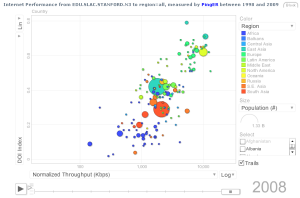

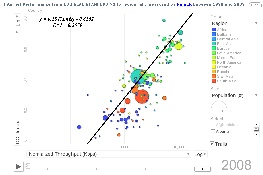

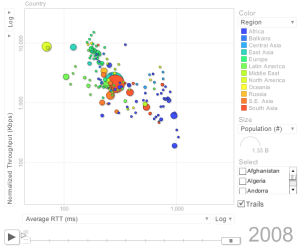

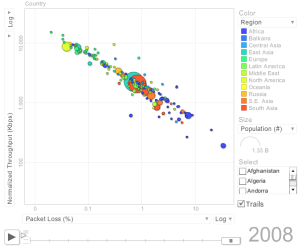

Motion Chart |

Motion Chart |

|---|---|

|

|

Recommendations

OECD Information Technology Outlook 2008: Highlights

Top ten ICT policy priorities, 2008

1 Government on line, government as model users

2 Broadband

3 ICT R&D programmes

4 Promoting IT education

5 Technology diffusion to business

6 Technology diffusion to individuals and households

7 Industry-based and on-the-job training

8 General digital content development

9 Public sector information and content

10 ICT innovation support

IHY, eGY, IST Recommendations

- Recognize: can't fix all ills for all people over night.

- Identify focus areas:

- educate teachers & students, attract research (reverse brain drain)

- applications: e.g. education, telemedicine, distance learning ...

- Find energetic leaders from country/region

- Engage policy makers for science, technology, education ...:

- Encourage ICT development, Internet adoption

- Collaborate between institutions, regions to increase leverage

- Form partnerships with vendors & providers:

- Drive market penetration, create demand, long term investments...

- Get support: funding agencies, diaspora, organizations like IHY, eGY, ICTP, professional societies ...

- Make & use measurements to illustrate case for improvement

- Acknowledge need for new business models appropriate for region

EU AU JOINT STATEMENT ON IMPLEMENTATION OF THE EU-AU PARTNERSHIP FOR SCIENCE, INFORMATION SOCIETY AND SPACE.

There are 2 projects under the information society priority

- Africa Connect

- The AfricaConnect project will support the development of regional research and

education networks in Sub-Saharan Africa and their interconnection with the European

GEANT2 network, building on a similar initiative, EumedConnect, implemented in North-

Africa (currently interconnecting around 1,5 Million users across more than 500 research

organisations). The objective will be to contribute integrating the African research

community both at regional and international levels, through interconnection with the most

cost-effective high bandwidth capacity.

- The AfricaConnect project will support the development of regional research and

- The African Internet Exchange System (AXIS)

- This project aims to support the establishment of a continental African internet

infrastructure through national and regional internet exchange points. Such

deployment is considered crucial for the development of the internet in Africa,

generating huge costs savings by keeping local traffic local and offering better quality

of service and new applications opportunities. AXIS activities will include technical

assistance on planning,

- This project aims to support the establishment of a continental African internet

Business Issues

According to Vital Wave Consulting, there are:

Three Inhibitors to Emerging Market Success

- Multinational corporations want to grow revenues in emerging markets, but their success is threatened by deeply ingrained practices tailored to the mature-market environment:

- Corporate incentive structures favor short-term performance over longer-term business investment and execution

- Technological innovation overshadows new business models

Reliance on traditional data sources and market analyses that misrepresent developing-country business opportunities.

also offer:

solutions that suit shared-use computing environments (e.g., government offices, schools, SMBs, Internet cafés, and community centers). The challenge in these settings is to provide a genuine PC experience to more people for the lowest cost per computing terminal.

The saturation of Internet penetration, broadband use etc. in developed countries is not happening for developing countries (see for example Emerging Countries Start to Move up the Broadband ranks and World Broadband Statistics Q3 2008). This is despite the current mixture of financial meltdown, recession, the threat of deflation, global apocalypse etc.

News

Orange to link Madagascar to broadband internet via a new submarine fibre optic cable Paris, March 26, 2008, from Mike Jensen

France Telecom & Orange plan to install a submarine fibre optic cable

providing Madagascar with broadband internet. Known as Lion, the 1,800 km cable will connect Madagascar with the region's existing Sat3-Wasc-Safe cable.

Lion will link Madagascar with the rest of the world via the islands of Reunion and Maurice, the two connection points of the Sat3-Wasc-Safe cable, which itself links Europe to Asia via South Africa. The investment will be made by a consortium including Orange Madagascar, Mauritius Telecom, and France Telecom who will operate the cable jointly. The consortium could later be extended to include other partners.

The investment falls in line with the development policy programmed by the state of Madagascar. It covers the purchasing, the installation of the submarine cable, the construction of a landing station in the region of Toamasina, and a very high speed fibre optic link from Toamasina to the capital.

The submarine cable Lion will contribute to the development of the telecommunications network, a determining factor in the social and economic development of the region. This new very high speed cable provides an excellent international connection for internet-based activity.

For more see http://www.francetelecom.com/en_EN/press/press_releases/cp080326-uk.html.

According to Mike Jensen (priv comm)

Perhaps this is good news for Madagascar, but too early to tell...as it stands now they'll still have to connect upstream to the costly and unreliable SAFE..but there is also rumour that TEAMS will head down to Mauritius, so if that happens then there will be much better upstream bandwidth for madagascar/mauritius/reunion... so yes, SAT3/SAFE is still run on old business model and limited capacity, hopefully it will finally get some real competition!

SEACOM to launch Africa undersea cable June 2009

Reuters, Thursday August 14 2008

JOHANNESBURG, Aug 14 (Reuters) - Mauritius-registered private equity venture SEACOM said on Thursday a fibre optic undersea cable linking east Africa to Europe and Asia would be launched in June 2009, in time for the 2010 soccer World Cup.

The company said in a statement it would start laying the $650 million cable, which is needed to provide high-speed Internet access and spur investment, in October this year.

The 15,000 km cable will wind around the east of the continent between South Africa and Egypt, then on to Mumbai in India and Marseille in France. The group will start connecting sections of the cable in April 2009.

"The team is also trying to expedite the construction in an attempt to assist with the broadcasting requirements of the FIFA Confederations Cup scheduled for June 2009," SEACOM said.

The cable will provide 1.28 terabits per second of broadband capacity to enable high definition TV and provide inexpensive bandwidth.

SEACOM said last year investors in the venture included an arm of the Aga Khan Fund for Economic Development, Venfin Ltd. and Herakles Telecom LLC, each with a 25 percent stake, and Convergence Partners with a 12.5 percent shareholding.

The Shanduka Group, owned by South African black business tycoon Cyril Rhamaphosa, holds the remaining 12.5 percent.

Nedbank Capital, a division of Nedbank and Investec Bank are funding the project.

South Africa's second telephone network operator, Neotel NEO.UL, which is competing with former monopoly Telkom has secured the rights to control the cable's use in South Africa.

South Africa has only one cable linking it to the rest of the world and this was controlled by Telkom until Sept. 2007. (Reporting by Gugulakhe Lourie; editing by Tony Austin)

Google & Satellite coverrage (September 2008)

Google announced this week that it was involved in a radical new plan to bring internet access to the majority of the developing world.

The internet giant has signed up with Liberty Global and HSBC in a bid to launch 16 satellites, which will bring high-speed internet access to Africa and parts of Asia, Latin America, Australia and the Middle East.

The project aims to use low earth orbit satellites instead of fibre cables for the core network, which will link to cellphone towers throughout the developing countries.

This is great news for the telecoms and broadband industry in South Africa, where new players are looking to get into the market to provide some much-needed competition.

The project, which has been dubbed the 03b Network, named after the "other three billion" people for whom fast fibre internet access networks are not commercially viable, is set to come online by the end of 2010.

The 16 satellites will be able to cover all points between 45° north of the equator and 45° south of the equator.

A recent World Bank report titled Broadband for Africa: Policy for promoting the development of backbone networks says the average retail price for basic broadband in sub-Saharan Africa in 2006 was US$366 a month, while in India it was US$44, in Europe US$40 and in the United States US$12.

The report says the major reason for this is the lack of high-quality backbone infrastructure that would allow for affordable mass-market broadband access.

EU-AU Partnership (October 6, 2008)

The African Union Commission and the European Commission have issued a joint statement on the implementation of the EU-AU partnership for science, information society and space.

Among the 19 flagship projects that have been identified, 2 in the field of ICT are ready for early implementation (Africa Connect and the African Internet Exchange System).

The statement can be downloaded at http://www.euroafrica-ict.org/downloads/EU-AU_Joint_Statement_Final_EN_EU.pdf.

Fibre project finished in Botswana

30/10/2008 The multi-million Pula Trans-Kalahari fibre-optic project was recently completed in Botswana. Covering approximately 2000km, the project is expected to act as a catalyst to the growing ICT industry in the country.

Africa's first communications satellite fails (Science and Development Network (November 17, 2008)

By Adole Hassan

ABUJA Africa's first communications satellite has suffered an energy failure just 18 months after its launch.

The NIGCOMSAT-1 satellite was launched from China in 2007 (see Satellite launches boost African communications) amidst optimism that it would aid development by linking up rural communities and progressing telemedicine and long-distance learning. There were also ambitious commercial goals. But these are now dashed, say commentators. The 40 billion Nigerian Naira (US$240 million) satellite was entirely government-owned but was "fully insured," said Rufai.

A geostationary satellite, it was supposed to work for 15 years, and is officially monitored by a ground control station in Abuja, Nigeria, with backup stations in China, Italy, northern Nigeria and the Council for Scientific and Industrial Research (CSIR) satellite applications centre in Hartebeesthoek, South Africa.

Zaku told SciDev.Net that Internet service providers in Nigeria and telecommunications companies who were using the satellite would be moved to other satellites if engineers confirm that it is unfixable.

Other Digital Divides

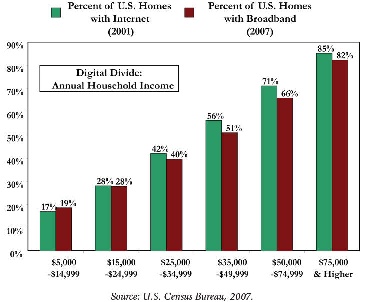

Economic Digital Divide

As seen below in the graph (from Down Payment on Our Digital Future ) of percent of US homes with the Internet in 2001 and Broadband in 2007 there is a economic digital divide.

A Typology of Information and Communication Technology Users

This sorts Americans into 10 distinct roups of uses of communication and information technology. It shows that:

Some 15% of Americans have neither a cell phone nor internet access. They tend to be in their mid-60s, nearly three-fifths are women, and they have low levels of income and education. Although a few have computers or digital cameras, these items seem to be about moving digital information within the household - for example, using the computer to display digital photos that they take or others physically bring into the house.

Presentations etc.

- "The Strategic importance and impact of e-infrastrucures for Science, Society and Economy in Europe and neighbouring Southern Countries", Robert Klapisch, EUMED 2008, Amman, Jordan 2008

- Digital Divide in Sub-Saharan African Universities: recommendations and monitoring, by B. Barry, M. Petitdidier, L. Cottrell, C. Barton for the IST-Africa conference and exhibition, May 07-09, 2008 Windhoek, Namibia.

- Internet Connectivity in Africa, presented by Les Cottrell at the Internet and Grids in Africa: An Asset from African Scientists for the Benefit of African Society, 10-12 December 2007, Montpellier France.

- January 2008 report of the ICFA-SCIC monitoring Working Group

- Telegography Telecoms International Workshop, Tim Stronge, Eric Schoonover at PTC'08 13-16 January 2008

- GLOBAL BANDWIDTH RESEARCH SERVICE EXECUTIVE SUMMARY, Telegeography

- "Spiralling bandwidth demands spur undersea cable deployment", Joel Hruska, ARSTechnica, July 2008

- "Internet-led demand puts cable-laying at top of list", Paul Yaylor, Financial Times July 8, 2008

- "Emerging Markets Definition and World Market Segments ", Vital wave, 2009.